Building Long-Term Wealth: Essential Foundational Concepts for Financial Success

🌱 1. The Wealth Mindset & The Magic of Compound Interest

Welcome to your first step toward true financial freedom! 🚀 Building long-term wealth isn’t about overnight success; it’s about establishing a solid foundation that works for you over time. First, we must shift our mindset from short-term spending to long-term investing. Have you ever wondered how the truly wealthy get there? It all starts with understanding compound interest, which Albert Einstein famously called the eighth wonder of the world. Compound interest is simply earning interest on your interest, creating a snowball effect for your money. To harness this power, you must start early because time is your greatest ally in the market. Imagine putting away just a small amount today and watching it grow exponentially over decades! This foundational concept requires patience, discipline, and a shift in perspective. Here are three key habits to build this mindset:

- Pay yourself first by saving a portion of your income before spending.

- Stay consistent by automating your savings to remove emotional decision-making.

- Think long-term by ignoring daily market noise and focusing on your decades-long horizon.

By prioritizing consistency over intensity, you set the stage for your money to work tirelessly on your behalf.

💰 2. Mastering Cash Flow: The Fuel of Wealth Generation

You cannot build an impressive financial fortress if you have leaks in your foundation. That is why mastering your cash flow through strategic budgeting is absolutely essential for your long-term success. Many people dread the word ‘budget,’ but you should view it as a tool of empowerment rather than restriction. A budget does not tell you what you cannot spend; rather, it gives your money a clear direction and purpose. To build wealth, your primary goal must be to increase the gap between what you earn and what you spend. This surplus is your investment capital—the raw fuel that accelerates your wealth-building engine. When you track your expenses, you gain complete visibility over your financial health. It allows you to make conscious choices aligned with your ultimate goals. You must also learn to distinguish between assets (things that put money in your pocket) and liabilities (things that take money out). Living below your means is the golden rule of finance, regardless of how much your salary increases. Let’s look at the classic 50/30/20 rule to simplify your cash flow management:

- Fifty percent of your income goes to essential needs like housing and utilities.

- Thirty percent is dedicated to your personal wants and lifestyle spending.

- Twenty percent goes directly to savings, debt payoff, and investments.

By taking control of where every dollar goes, you transition from a passive spender to an active wealth creator.

🛡️ 3. Establishing Your Safety Net: Debt Elimination and Emergency Reserves

Before you dive headfirst into investing, you must build a robust shield to protect your growing wealth. The first line of defense is creating an emergency fund of three to six months’ worth of living expenses. This fund acts as your financial cushion, ensuring you do not have to liquidate investments or take on bad debt when life throws unexpected curveballs, like medical issues or sudden job loss. The second crucial step is aggressively paying down high-interest consumer debt, such as credit card balances. High-interest debt is a wealth-killer that drains your monthly cash flow and actively works against compounding. Think about it: why invest for an 8% return when you are paying 20% on a credit card? Paying off high-interest debt is equivalent to earning a guaranteed, tax-free return equal to your interest rate! This strategy immediately frees up cash to put toward your long-term goals. By systematically clearing what you owe, you reclaim your purchasing power. This foundational security is what allows you to take calculated risks later. To achieve this quickly, consider these two popular debt-paydown methods:

- The Debt Avalanche method targets paying off debts with the highest interest rates first to save money.

- The Debt Snowball method focuses on paying off the smallest balances first to build psychological momentum.

Once your high-interest debt is gone and your reserve is funded, you are officially ready to play offense.

📈 4. Intelligent Investing: Asset Allocation & Diversification

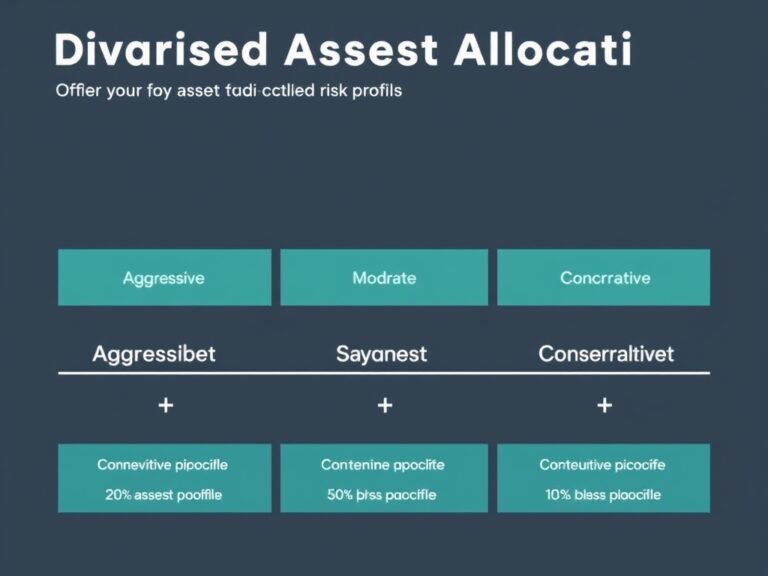

Now that you have built your safety net, let’s explore how to grow your wealth through intelligent investing. Investing is not about gambling or picking the next trending meme stock; it is about building a diversified portfolio. Diversification is the practice of spreading your investments across various asset classes, such as stocks, bonds, and real estate, to minimize risk. By diversifying, you ensure that a downturn in one sector won’t devastate your entire life savings. Your ideal asset allocation should reflect your personal risk tolerance and your specific timeline. For instance, younger investors can generally afford to take more risks because they have time to recover from market fluctuations. Conversely, those nearing retirement often shift toward safer, income-generating assets to protect their capital. A great way to start is with low-cost index funds, which allow you to buy a small slice of hundreds of companies simultaneously. This hands-off approach outperforms most active stock pickers over the long run. It also saves you countless hours of stress and analytical fatigue. To manage your portfolio effectively, focus on these three core investing pillars:

- Asset allocation balances risk and reward by adjusting your portfolio mix over time.

- Diversification spreads your money across different companies, industries, and geographic regions.

- Low costs ensure you keep more of your returns by choosing low-expense index funds.

Consistent, automated investing over time will always yield better results than trying to time the market.

🎯 5. Lifelong Learning & Staying the Course

Finally, the ultimate driver of long-term wealth is your dedication to continuous personal growth and financial literacy. The financial landscape is constantly evolving, and staying informed is your greatest competitive advantage. This doesn’t mean you need a finance degree, but reading books, listening to reputable podcasts, and understanding economic trends will keep you sharp. Moreover, building wealth is as much a psychological challenge as it is a mathematical one. During market downturns, the media often panics, tempting you to sell your investments at a loss. True wealth builders understand that market corrections are normal and represent buying opportunities rather than disasters. Discipline and emotional control are what separate successful investors from the rest. By staying the course and ignoring temporary market volatility, you ensure your long-term strategy remains intact. Remember that wealth is built slowly and steadily over years, not days. Let’s summarize the key rules to live by on your journey to financial freedom:

- Stay educated by spending at least thirty minutes a week reading about personal finance.

- Keep emotions in check so you never make hasty decisions during market highs or lows.

- Review your goals periodically to ensure your plan still aligns with your evolving life.

Your future self will thank you immensely for the smart, disciplined choices you make today.