Foundational Principles for Building Long-Term Wealth: A Strategic Guide

Mastering Your Financial Foundation: Why Long-Term Wealth Starts Today

Building genuine long-term wealth isn’t about hitting a lucky lottery ticket or finding a magical stock that turns ten dollars into a million overnight. Instead, it is a deliberate, strategic game of consistency, discipline, and understanding the core mechanics of compounding interest. Think of your financial future as an oak tree; you plant the seed today, water it with regular contributions, and nurture it through the stormy markets of life. Most people fail because they lack patience or a clear roadmap, yet the principles of wealth building remain surprisingly simple to grasp. By focusing on your cash flow and debt reduction early on, you set the stage for your assets to actually work for you rather than against you.

- Mindset Shift: Stop seeing money as something to spend, and start viewing it as a tool.

- Consistency: Small, automated habits beat large, infrequent bursts of activity every single time.

- Clarity: Define exactly what ‘wealth’ means to you, whether it is early retirement or financial freedom for your children.

Achieving financial success is a marathon, not a sprint, and your success depends entirely on how well you manage your resources during the early miles. Are you ready to stop chasing quick wins and start building a legacy that lasts for decades? Let’s dive into the foundational pillars that every successful investor needs to master to navigate the path toward sustained financial prosperity.

The Art of Strategic Budgeting and Cash Flow Management

You cannot effectively grow what you cannot control, which makes strategic budgeting the absolute bedrock of your wealth-building journey. Many people recoil at the word ‘budget,’ viewing it as a restrictive cage that prevents them from enjoying life, but it is actually a roadmap for freedom. When you track every dollar, you gain the power to consciously allocate funds toward income-generating assets instead of depreciating liabilities. It is not about depriving yourself of daily joys like that morning coffee; it is about ensuring those joys don’t cannibalize your long-term goals. By categorizing your expenses and automating your savings, you remove the emotional burden of decision-making from the process. Consider using the 50/30/20 rule: 50% for needs, 30% for wants, and 20% for your future self.

- Automate Everything: Use bank settings to move savings into investments automatically.

- Audit Regularly: Once a month, review where your capital is leaking and plug those holes.

- Increase Savings Rate: As your income grows, try to keep your lifestyle constant to maximize the surplus.

Mastering your cash flow is essentially the engine that powers your investment portfolio, and without it, even the smartest investment strategies will eventually sputter out. Remember, the goal is to widen the gap between your income and expenses, creating the fuel necessary for compounding to work its magic over the coming years.

Leveraging Compounding: The Investor’s Secret Weapon

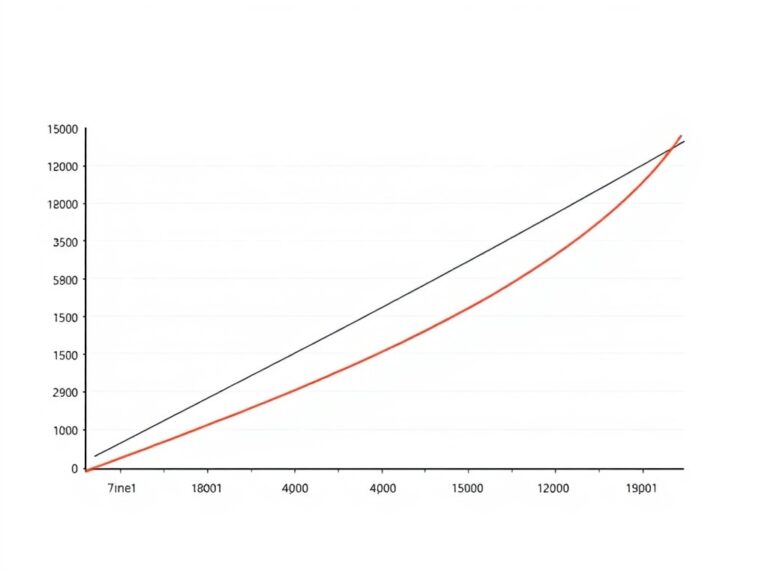

Albert Einstein reportedly called compounding interest the eighth wonder of the world, and for good reason—it is the closest thing we have to a financial superpower. When you invest, your earnings start generating their own earnings, creating a snowball effect that grows exponentially the longer it rolls down the mountain. The key to capturing this magic is time in the market, which is far more valuable than trying to time the market perfectly. Diversification acts as your guardrail, ensuring that a temporary decline in one sector doesn’t derail your entire plan. You don’t need a Wall Street degree to succeed; you just need to keep costs low by utilizing index funds or ETFs.

- Start early, even if you are just contributing small amounts at first.

- Avoid frequent trading; let your investments sit and do the heavy lifting for you.

- Understand that market volatility is a feature, not a bug, of wealth accumulation.

If you start investing in your twenties, your dollars have decades to multiply, turning relatively modest contributions into significant wealth by the time you reach retirement. The longer you wait, the more you have to invest to reach the same result, making time your most precious and limited asset. Always remember that your goal is to stay invested through the ups and downs, as consistent participation is the primary driver of superior long-term performance in any asset class.

Protecting Your Legacy: Risk Management and Future Planning

Finally, building wealth is only half the battle; the other half is protecting the wealth you have worked so hard to accumulate. Life is inherently unpredictable, and a single emergency—whether it is a health crisis or a sudden job loss—can wipe out years of progress if you aren’t properly prepared. An emergency fund covering three to six months of expenses is non-negotiable for anyone serious about their long-term financial security. Beyond that, you need to consider insurance as a strategic tool, not just an added expense, to shield your assets from liability. Estate planning, even at a young age, ensures that your hard-earned assets go exactly where you want them to go without unnecessary legal interference.

- Establish a safety net before taking risks with speculative investments.

- Review your insurance policies annually to ensure coverage matches your growing net worth.

- Create an estate plan that includes a will and beneficiary designations to protect your legacy.

Taking these steps might not seem as exciting as picking the next big stock, but they are the bedrock that prevents a crisis from becoming a catastrophe. By removing the fear of the unknown from your financial picture, you can make smarter, more objective decisions about your growth strategies. True financial peace of mind comes when you know that no matter what the world throws at you, your foundation remains solid, protected, and ready to continue growing into the future.