The Core Foundations of Long-Term Wealth Building You Need to Master

Have you ever wondered why some people seem to build wealth effortlessly while others constantly struggle paycheck to paycheck? The truth is, building long-term wealth isn’t just about how much money you make; it starts with a fundamental shift in your wealth mindset. Cultivating a healthy relationship with money means moving away from instant gratification and embracing the power of delayed satisfaction. 🧠 Wealth building is a marathon, not a sprint, and mastering your psychology is the absolute first step on this journey. When you view money as a tool for freedom rather than a status symbol, your spending and saving habits naturally align with your long-term goals. This mental shift allows you to distinguish between assets that put money in your pocket and liabilities that take it out. To truly master this foundation, you must commit to continuous financial education and cultivate a belief that your financial destiny is within your control.

- Understand the difference: Wealth is what you don’t see—it’s the saved and invested capital, not the flashy cars or luxury items.

- Shift your focus: Shift from a consumer mindset to an investor mindset, prioritizing long-term security over short-term thrills.

- Define your ‘Why’: Knowing exactly why you want to build wealth keeps you motivated when market fluctuations or lifestyle temptations arise.

By establishing this rock-solid psychological foundation, you pave the way for all the practical financial strategies that follow. Remember, your mind is your most valuable financial asset, so nourish it with knowledge and discipline daily. Ultimately, mastering your mindset transforms how you perceive opportunities and risks, preparing you for sustainable financial growth.

Once your mindset is aligned, the next critical pillar of wealth creation is mastering your cash flow through strategic budgeting. You cannot build a lasting financial house on a shaky foundation of unmonitored spending and rising high-interest debt. Managing your cash flow effectively means knowing exactly where every dollar comes from and, more importantly, where it goes. 📊 Utilizing a structured approach, like the popular 50/30/20 rule, can help you allocate your income efficiently without feeling deprived.

- 50% for Needs: This portion is dedicated to essential living expenses such as housing, utilities, groceries, and insurance.

- 30% for Wants: This portion covers discretionary spending including dining out, hobbies, entertainment, and personal shopping.

- 20% for Savings & Debt: These crucial funds are allocated toward emergency savings, retirement accounts, and aggressive debt payoff.

Additionally, building an emergency fund containing three to six months of living expenses acts as a vital financial buffer. This liquid safety net ensures that unexpected life events, such as medical bills or job loss, do not force you into high-interest debt. Remember, a budget is not a financial straightjacket; rather, it is a tool that gives you permission to spend mindfully while securing your future. By consistently maintaining a positive cash flow, you generate the vital surplus capital needed to fund your investment engines. Tracking your net worth monthly will keep you highly motivated as you watch your debts shrink and your cash reserves expand. Consistently spending less than you earn is the simplest, yet most profoundly impactful, formula for generating sustainable wealth.

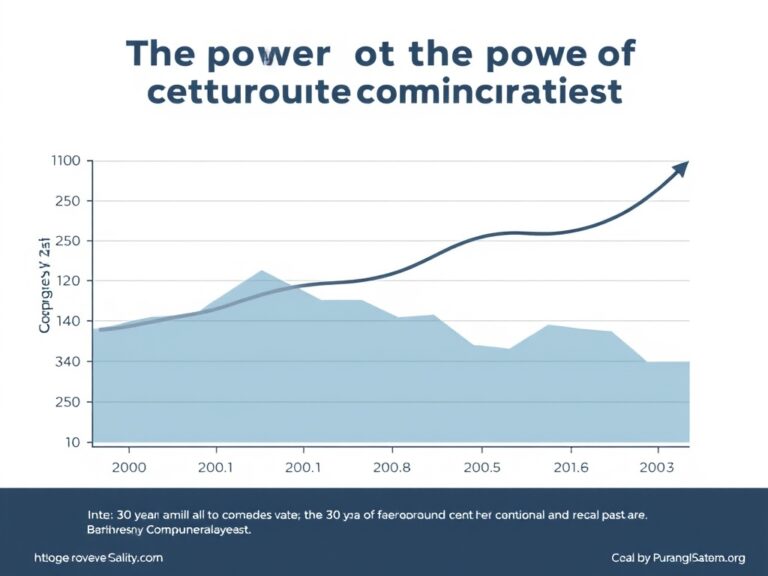

With a healthy cash surplus secured, you are now ready to harness the single most powerful force in finance: compound interest. Often referred to by Albert Einstein as the eighth wonder of the world, compounding is the process where your earnings generate their own earnings. Over time, this compounding effect snowballs, turning modest, regular contributions into an absolute mountain of wealth. ⏳ The key ingredient that unlocks this magical process is time, which is why starting to invest as early as possible is so paramount. Even small amounts invested in your twenties can easily outperform much larger sums invested later in life due to the power of compounding. To illustrate this, consider how consistent, long-term investments in diversified index funds historically yield excellent returns over several decades.

- Start Early: Time is your greatest ally because a dollar invested today is worth far more than a dollar invested tomorrow.

- Reinvest Dividends: Automatically reinvesting your investment dividends accelerates the compounding process exponentially.

- Stay the Course: Avoid the temptation to time the volatile market, and instead rely on the proven power of time in the market.

By automating your investments, you remove emotional decision-making and ensure you consistently buy assets regardless of short-term market noise. This disciplined approach leverages dollar-cost averaging, allowing you to acquire more shares when prices are low and fewer when they are high. Over a multi-decade horizon, compound interest does the heavy lifting for you, transforming your active labor into passive wealth. Ultimately, understanding and respecting this mathematical phenomenon is what separates casual savers from truly wealthy individuals.

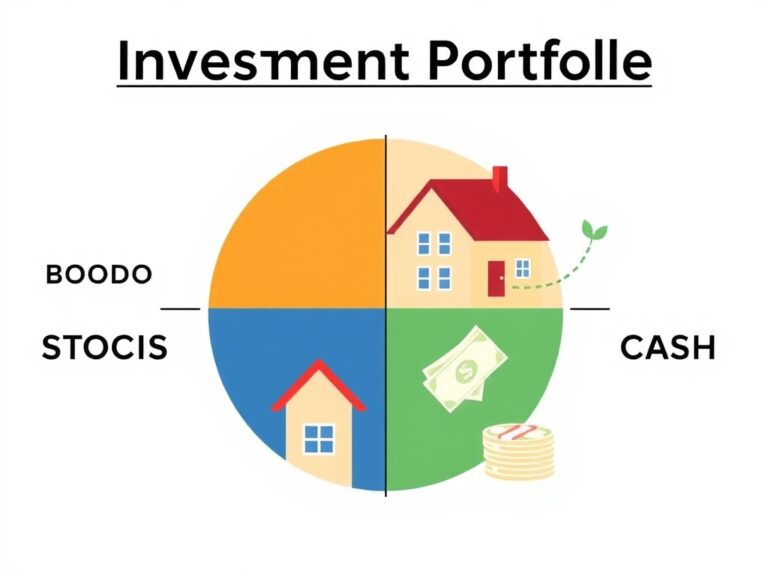

As you begin investing your hard-earned money, you must understand the vital role of asset allocation and diversification. Diversification is the financial equivalent of not putting all your eggs in one single, fragile basket. By spreading your capital across various asset classes, you drastically reduce your portfolio’s overall risk while optimizing potential returns. 📈 A well-diversified portfolio typically includes a balanced mix of equities, fixed-income bonds, real estate, and perhaps alternative investments. Equities provide strong long-term growth potential, whereas bonds offer stability and steady income, helping to smooth out volatile market cycles. Real estate can act as a fantastic hedge against inflation, providing both physical equity and consistent rental cash flow over time.

- Stocks/Equities: These assets offer high growth potential but are accompanied by higher short-term market volatility.

- Bonds/Fixed Income: These assets provide lower growth potential but offer predictable income streams and capital preservation.

- Real Estate: This asset class offers tangible asset value, unique tax advantages, and potential for long-term rental income.

Your specific asset allocation should always align with your unique risk tolerance, financial goals, and investment time horizon. Younger investors might opt for a more aggressive, stock-heavy portfolio, while those nearing retirement often transition toward conservative, income-generating assets. Regularly rebalancing your portfolio ensures that your asset mix stays aligned with your target risk profile as market values fluctuate. Embracing strategic diversification protects your hard-earned wealth from catastrophic losses and guarantees more predictable, long-term growth.

The final, yet frequently overlooked, pillar of mastering long-term wealth building is protecting your assets through tax efficiency and insurance. It is not just about how much money your investments make, but how much of those earnings you actually keep. Utilizing tax-advantaged accounts, such as 401(k)s, IRAs, or HSAs, can save you thousands of dollars in taxes over your lifetime. 🛡️ Additionally, protecting your growing wealth requires a comprehensive risk management strategy, which includes having the right insurance policies. Without adequate health, life, disability, and property insurance, a single catastrophic event could wipe out years of diligent financial progress. Estate planning is another critical component, ensuring your hard-earned assets are distributed according to your wishes without excessive legal delays.

- Maximize Tax Shelters: You must actively contribute to retirement accounts to reduce your current taxable income and grow wealth tax-free.

- Obtain Proper Insurance: You should protect your earning capacity and physical assets against unforeseen, high-cost emergencies.

- Create an Estate Plan: You need to draft a will and establish trusts to seamlessly protect and transition your wealth to future generations.

Consult with certified financial planners and tax professionals to tailor these complex strategies specifically to your unique life situation. By proactively shielding your assets from taxes and unpredictable risks, you ensure that your financial legacy remains intact for decades. Wealth preservation is just as critical as wealth creation, and ignoring this truth can lead to devastating financial setbacks. Master these core foundations today, and you will build an unbreakable financial fortress that serves you and your family for a lifetime.