7 Foundational Principles for Building Long-Term Wealth and Financial Freedom

Mastering Your Financial Foundation: A Roadmap to Wealth

Building long-term wealth isn’t about chasing the next get-rich-quick scheme; it’s about consistent habits and a mindset shift that favors the long game over instant gratification. To achieve true financial freedom, you must first treat your personal finances like a business, tracking every dollar that flows in and out of your accounts. Think of your current financial state as the soil; if you plant seeds of discipline today, you will harvest the fruits of security tomorrow. The first step involves creating a zero-based budget, where every dollar has a specific job before the month even begins. This ensures that your spending aligns perfectly with your goals, preventing the common trap of ‘lifestyle creep’ as your income grows. By prioritizing essential expenses while ruthlessly cutting unnecessary subscriptions, you gain immediate control over your cash flow. Remember, the goal isn’t deprivation, but rather intentionality in how you allocate your resources. When you consciously decide where your money goes, you regain the power to direct it toward assets that appreciate rather than liabilities that drain your wealth. Start by assessing your current net worth—assets minus liabilities—to establish a clear baseline for your journey. This fundamental awareness is the catalyst that transforms ‘wishing’ into a strategic ‘doing’ phase of your life.

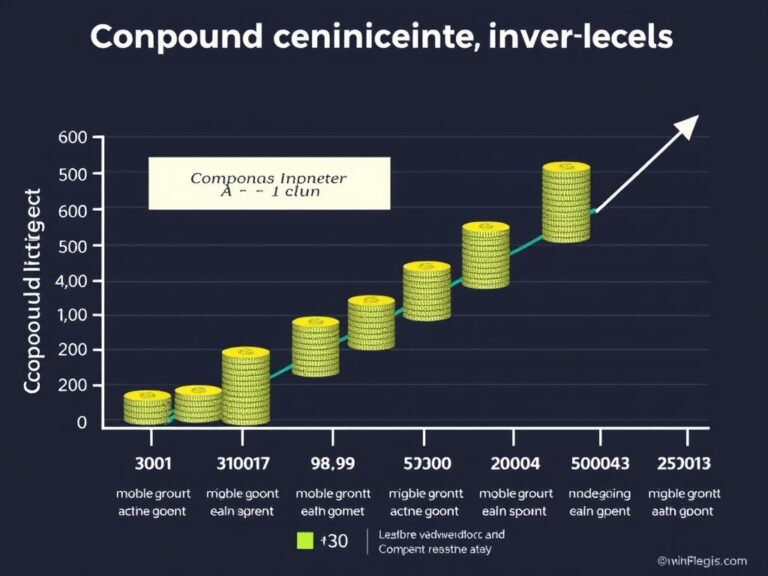

The Power of Compounding and Strategic Savings

Once your budget is established, the magic of compound interest becomes your greatest ally in building a fortune. It is often described as the ‘eighth wonder of the world’ because it allows your money to grow exponentially over time, provided you give it enough room to work. You should aim to automate your savings, treating your investment contributions like a non-negotiable monthly bill. By paying yourself first, you ensure that you are prioritizing your future self before the world has a chance to take its cut. Emergency funds act as a critical safety net, shielding your long-term investments from the need to be liquidated during life’s inevitable curveballs. Ideally, aim for 3 to 6 months of living expenses tucked away in a high-yield savings account that is separate from your daily checking. This separation is crucial for psychological reasons; it makes the money less accessible for impulse purchases while remaining liquid enough for true emergencies. Furthermore, understand that inflation is a silent tax on cash sitting idle, making strategic investing essential for maintaining and growing your purchasing power. Don’t wait for the ‘perfect time’ to invest, as market timing is a myth; time in the market almost always beats timing the market. By consistently contributing to diversified accounts, you allow the snowball effect to turn small, steady deposits into a substantial retirement nest egg.

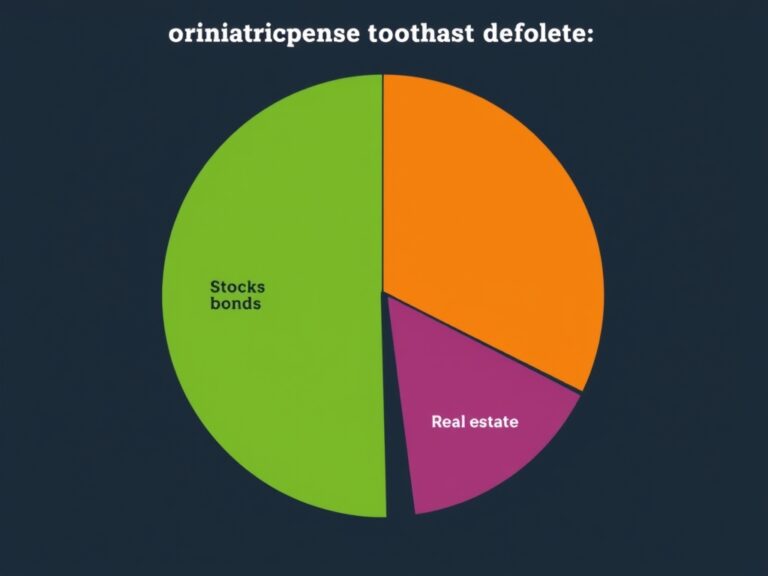

Diversification: The Only Free Lunch in Investing

As you begin to grow your wealth, you must embrace the principle of diversification to manage risk effectively. Putting all your eggs in one basket is a recipe for disaster, especially in volatile markets where sector-specific downturns can occur without warning. Instead, spread your investments across various asset classes like stocks, bonds, real estate, and index funds to ensure stability. An S&P 500 index fund or a total stock market ETF provides instant exposure to hundreds of companies, which minimizes the impact if one specific firm fails. This approach allows you to capture the growth of the broader economy while significantly smoothing out the bumpy ride of individual stock picking. Education is paramount here; take the time to understand the expense ratios of your funds, as high fees can eat into your compounded returns over decades. Remember, high-quality, low-cost index funds are often the best vehicles for building generational wealth for the average investor.

- Never invest in anything you do not understand.

- Use dollar-cost averaging to mitigate the impact of market volatility.

- Periodically rebalance your portfolio to maintain your desired risk tolerance.

By keeping your strategy simple and transparent, you avoid the complexity that leads to emotional decision-making. Your portfolio should reflect your long-term objectives, not the fear-based headlines of the daily news cycle, ensuring a steady path toward your financial goals.

The Final Pillars: Debt Management and Lifelong Learning

The final foundational principles revolve around strategic debt management and the relentless pursuit of financial literacy. Not all debt is created equal; bad debt, such as high-interest credit card balances, acts as a anchor that slows down your wealth-building speed. Focus on aggressively paying off these high-interest liabilities using either the ‘debt snowball’ or ‘debt avalanche’ method to free up cash flow. Conversely, good debt, like a low-interest mortgage or a student loan for a high-ROI degree, can sometimes be leveraged to build net worth over time. However, the ultimate goal should be total financial independence, where your passive income covers your living expenses entirely. To reach this stage, you must view your financial education as a lifelong endeavor rather than a one-time class. Stay curious by reading books, listening to reputable podcasts, and following market trends to adapt your strategy as life evolves. The landscape of finance changes, and those who remain flexible and informed are the ones who stay ahead of the curve. By minimizing your tax liabilities through retirement accounts like a 401(k) or IRA, you keep more of your hard-earned money working for you. Ultimately, true wealth is about buying back your time and having the freedom to pursue what truly matters to you. Stay disciplined, keep your vision clear, and remember that financial freedom is a marathon, not a sprint, where the greatest rewards go to those who remain persistent, patient, and prudent.